How to reprice diamond inventory without losing margin

Segment-aware diamond inventory repricing beats a portfolio average — when to reprice, which stones to lock, and how to read a session before you apply it.

A flat reprice run that pushes one monthly average across every row in your inventory will mis-quote two segments at once. April 2026 made the case in the open — bridal naturals trimmed roughly 2–3%, the investment tier held or rose, and the natural-over-lab-grown spread narrowed in the bridal band while widening above 2.00ct. Diamond inventory repricing that does not split the book by segment leaves margin on the floor in both directions, and the desk that applies a single anchor across the full inventory is the one that feels it at the invoice.

Why stale diamond prices leak margin

Margin leak from stale pricing is rarely uniform. It pulls in two directions at once: stones in a softening band sit above the live market and stop quoting, while stones in a firming band sit below it and quote profitably but under-price the desk's own cost-to-replace. A flat reprice using last month's portfolio average corrects neither cleanly — it nudges the whole curve and rounds off the boundary where the two regimes meet.

Platform listings vs bucket median — April 2026

The tiles read the current book as three slices: stones above tolerance against the live comparable (overpriced and likely sticking), stones below tolerance (under-priced and quoting through), and stones inside tolerance (no action). The split is the figure the desk actually works from — not a single "average drift" number that hides the directional spread between bridal and investment-tier rows. The April 2026 market report traced this divergence in detail, and the May reading has not collapsed the two regimes back into one.

A second source of leak is quieter. Locked stones — those on memo to a wholesale client, in an active parcel under contract, or held against a memo-back from a supplier — are not free to reprice this cycle. If the reprice session pushes them anyway, the recorded book value drifts away from the contractual price the desk will actually transact at, and the inventory report no longer matches the order book. The leak here is not a margin leak at the quote; it is a reporting drift that compounds over multiple cycles.

Which inventory segments to reprice first

Segment-by-segment sequencing matters more than reprice frequency. The bridal band — 1.00–2.00ct G–H VS1–VS2 natural rounds and their lab-grown comparable — is where weekly noise lives and where most volume sits in a typical dealer book. It needs the shortest reprice cycle and the tightest tolerance band on the move. The investment tier above 2.00ct D VVS1+ moves more slowly and absorbs portfolio-level averaging the worst — a 0.6% MoM print on D VVS1+ rows is real signal, and a flat reprice across the book washes it out.

| Reprice cadence | Anchor | Tolerance band | |

|---|---|---|---|

| Bridal natural rounds, 1.00–2.00ct G–H VS1–VS2 | Weekly | Natural-vs-lab-grown spread | ±2% |

| Lab-grown rounds, 1.00–2.00ct G–H VS1–VS2 | Weekly | Replacement cost | ±3% |

| Investment-tier natural, 2.00ct+ D VVS1+ | Bi-weekly | Natural-only benchmark | ±1.5% |

| Fancy shapes, 2.00ct+ | Monthly | Natural-only benchmark | ±3% |

| Slow-moving / aged inventory (>180 days) | Per quote | Manual review | n/a |

Sequencing the book this way changes what "the reprice ran" means in practice. A weekly bridal pass and a bi-weekly investment pass touch different parts of the inventory at different cadences, and the slow-moving rows do not see the reprice engine at all until a quote pulls them out. The reprice profile that anchors each segment to its own comparable is where the work actually sits — the cadence is a downstream choice. Create your pricing profile covers the configuration; the segment split above is what to configure it against.

The guardrails that keep repricing from becoming noise

A reprice run that moves every row, every cycle is not a reprice — it is a price-list overwrite. The guardrails that separate the two are the tolerance band, the per-bucket move cap, and the locked-stone list. The tolerance band defines the smallest move worth applying; setting it too tight produces sessions that flag the entire book and dilute the signal, while setting it too wide lets directional drift accumulate quietly across cycles. The values in the table above are starting points, not defaults — calibrate them against the noise floor of single-listing variance in each segment.

The per-bucket move cap is the protection against bad data on the input side. A snapshot with a thin comp set in a single bucket can return a 12% suggested move that reflects three outlier listings, not the market. Capping the per-cycle move at the magnitude the desk has historically seen on healthy comp sets — 3% on bridal, 2% on investment-tier — turns the cap into a flag rather than a fence: a row that hits the cap is asking for manual review, not a flat application of the suggested figure.

The locked-stone list is the third guardrail and the easiest to neglect. Memos, parcels under contract, consigned inventory, and supplier memo-backs all need an exclusion flag on the inventory record itself, not a downstream filter at the quote. A reprice that skips these by configuration is auditable; one that skips them by convention drifts the moment the convention is forgotten.

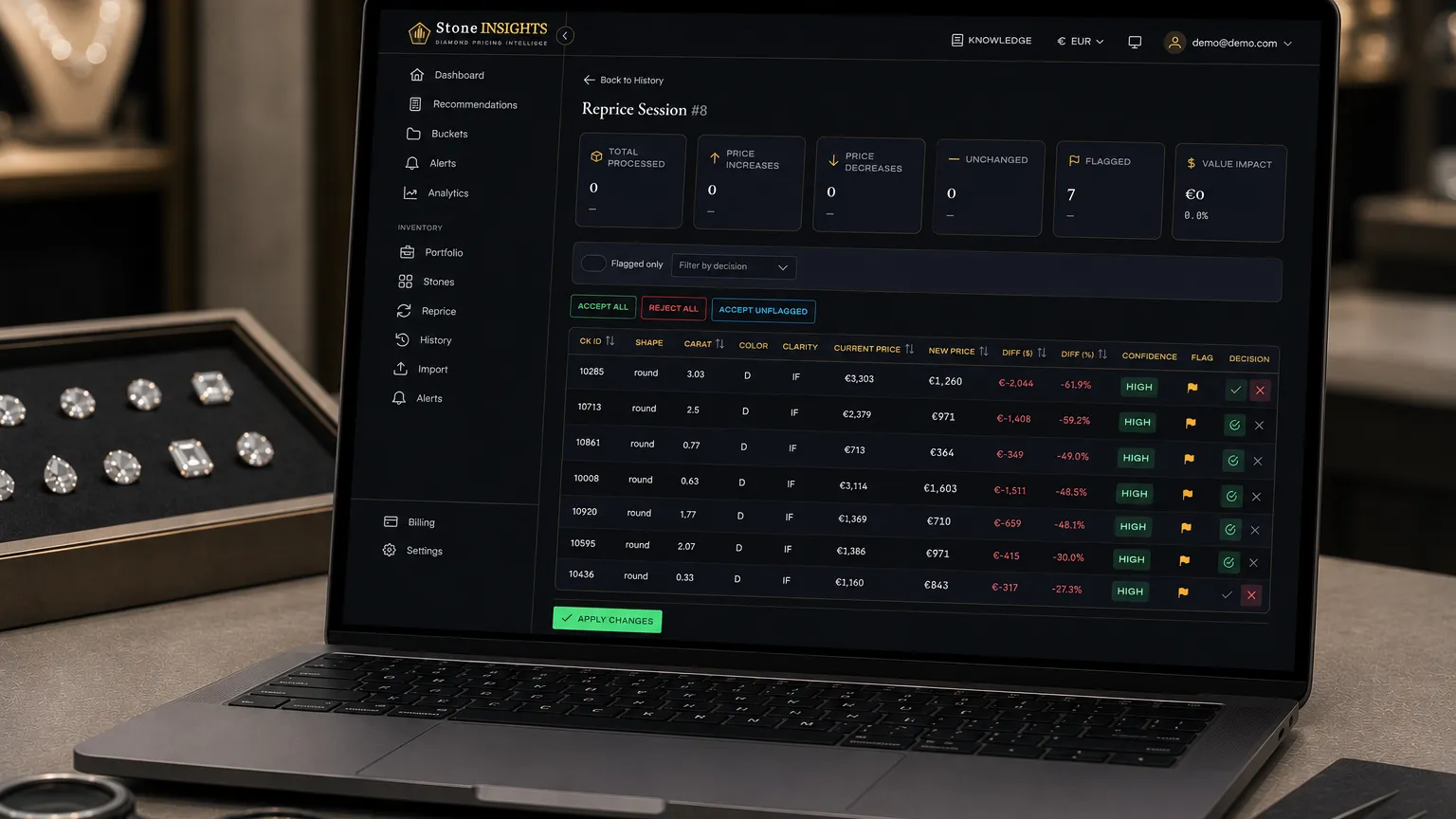

Reading the reprice session before you apply it

A reprice session is a draft, not a publish. The review step is where the segment view earns its cost. The bridal pass should show small directional moves clustered around the segment median — large outliers either resolve to genuine spec edge cases (a J SI2 priced from a thin comp set) or to a stale row the comp set has already moved past. The investment-tier pass should show fewer moves of smaller magnitude, and any row above the per-bucket cap deserves an explicit override decision, not a silent apply.

Avg price per carat by segment — Feb–Apr 2026

Round brilliant, EX cut, GIA paper. Bridal: G–H VS1–VS2, 1.00–1.99ct. Investment-tier: D VVS1+, 2.00ct+.

The chart traces the current book price against the suggested reprice band per segment. The shape to read for is whether the current curve sits inside the suggested band or has drifted to one edge. A book that has drifted to the upper edge across the bridal segments is the one above tolerance against the live market — the case for stones sticking on the quote sheet. A book that has drifted to the lower edge on investment-tier rows is the one under-pricing the resale narrative the buyer pool there actually pays for.

Two checks belong in every review. The first is the spread sanity check: pull the natural-vs-lab-grown spread on each bridal row and confirm the suggested move keeps the spread inside the band the April 2026 market report traced. A bridal row that suggests a move outside that spread is asking for either an override or a flag back to the comp set. The second is the investment-tier holdback: any row above 2.00ct D VVS1+ suggesting a downward move bigger than the per-bucket cap should hold for a second snapshot before applying. The investment tier moves on smaller comp sets and absorbs single-listing noise the worst.

The session-review mechanics — how to scope the run, apply selectively, and audit the change log — sit in Inventory and Reprice. The choices the desk makes inside that review are what this section covers.

When to schedule the next run

The reprice cadence is not a calendar choice; it is a coupling to the market reports the desk reads against. Each monthly market report on the platform sets a new baseline for the segment-level moves the reprice engine will pick up over the cycle that follows it, and the desk that schedules a session within the first 48 hours of each report consumes the new reading while the segment view is still freshest in the comp set. Off-cycle runs belong in two cases: a single-listing event large enough to move a bucket median — a parcel sale, a major supplier price card revision — and a desk-side trigger like a quote-through rate on a single segment crossing the desk's own threshold.

The repricing engine is a signal amplifier, not a market timer. The guardrails above are what keep the amplification clean — segment-by-segment anchors, tolerance bands calibrated to each segment's noise floor, per-bucket move caps, and locked-stone exclusions on the inventory record itself. A book repriced this way against a divergent market like April-to-May 2026 will quote correctly into both regimes without averaging across the boundary where they meet. The desk that defaults to the single-average reprice run is the one that has to take the next quote off the spreadsheet by hand.